TL;DR

- MiCA replaces legal uncertainty with harmonized EU crypto rules.

- German banks enter crypto via licensed custody and trading services.

- Authorization takes 12–18 months and costs €250k–€500k.

One year ago, Germany’s largest financial institutions would not touch crypto. DZ Bank, DekaBank, Commerzbank, and Deutsche Bank kept their distance. Compliance departments flagged every proposal as too risky. Boards refused to sign off. The lack of a clear legal framework made digital assets a liability for any traditional bank. Today, the same institutions offer crypto trading and custody services to millions of customers. The change happened fast. The driver is MiCA, the EU’s markets in crypto-assets regulation.

Matthias Steger, speaking: “MiCA was the door opener.” Before the regulation, German banks operated in a gray zone. No standardized rules meant each compliance review started from scratch. Lawyers gave conflicting opinions. Regulators offered no clear path. After MiCA, banks received a single rulebook valid across all EU member states. The legal uncertainty disappeared overnight.

Why MiCA opened the door for German banks

MiCA provides something banks value above almost anything else: regulatory certainty. The law defines exactly what a crypto-asset service looks like, what capital requirements apply, and how firms must handle customer assets. For a bank, compliance means checking boxes. MiCA supplies the boxes. The regulation also creates a level playing field. Any MiCA-licensed firm operates under the same rules, whether a small startup or Deutsche Bank.

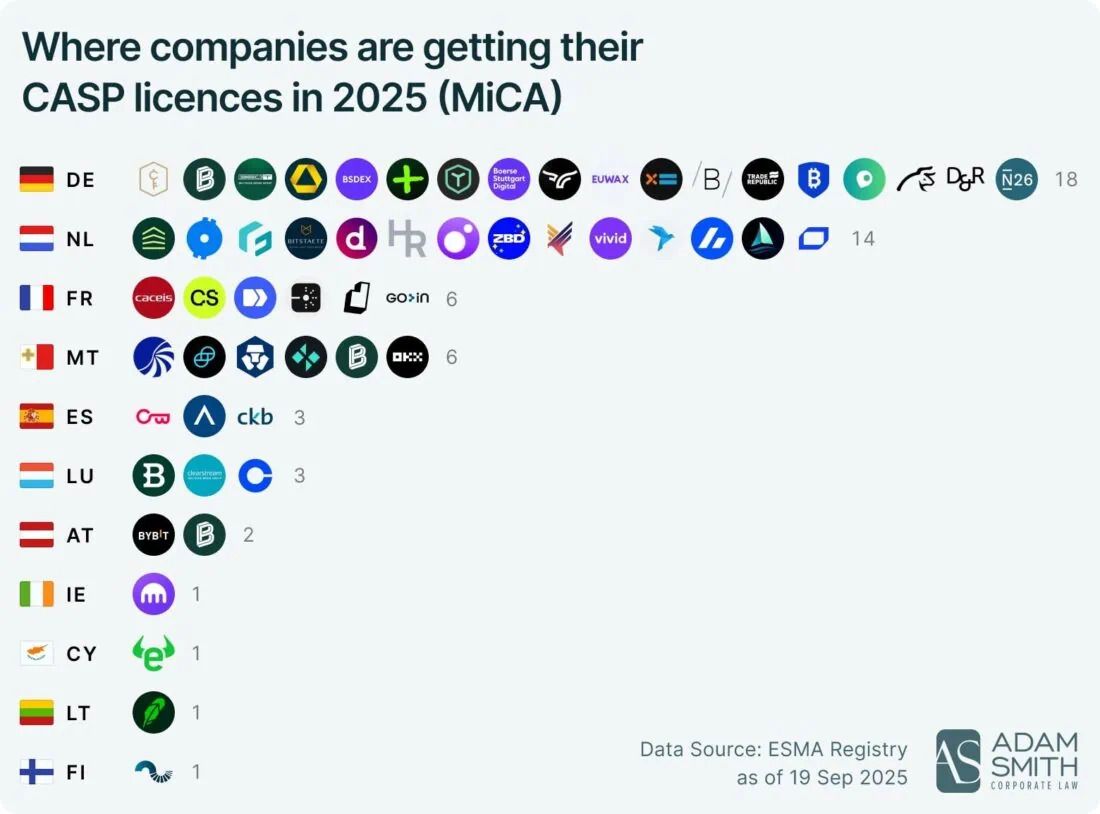

Germany’s cooperative giants and asset managers moved first. BaFin, the German regulator, approved multiple MiCA-aligned licenses in 2025 and 2026. Banks focused on low-risk entry points: custody and order execution. Retail customers can now buy and sell crypto through their existing banking apps. Institutional clients custody digital assets with their primary banking partner. Major custodians expanded services for institutions using infrastructure they already owned.

The numbers tell the story. Germany added 16 new MiCA-licensed institutions in the fourth quarter of 2025 alone. Most are traditional banks offering limited services. For these players, the approach is strategic: start small, build expertise, expand over time. MiCA-compliant platforms saw a 45% increase in institutional investments compared to non-compliant competitors. Banks point to their MiCA authorization as proof of compliance, attracting clients who previously avoided crypto entirely.

The same compliance requirements that burden startups work in favor of established banks. A startup might spend €250,000 to €500,000 on a MiCA license, a significant hit to its balance sheet. For a bank with billions in assets, the cost barely registers. Banks already employ legal teams, compliance officers, and capital reserves. Adding crypto services under MiCA uses existing infrastructure. Startups build everything from zero.

Holger Kuhlmann noted the pressure on smaller competitors: “Many companies have to make a decision between accepting more bureaucracy or taking on the cost and risk of relocation.” Banks face no such choice. They absorb the bureaucracy and use their scale as an advantage. Startups consider leaving Germany for Switzerland or the UAE. Banks double down on Frankfurt.

Critics of MiCA focus on its burden for smaller firms. The paperwork is real. The costs are real. Some startups will fail or relocate. But for institutional adoption, MiCA works exactly as designed. Germany may lose its crypto hub status among entrepreneurs. At the same time, German banks now treat digital assets as a legitimate asset class. Retail customers gain access through trusted interfaces. Institutional money flows into compliant platforms.

The entry of Germany’s largest banks into crypto represents a structural shift. Not a hype cycle. Not a speculative bubble. A permanent change driven by regulation. MiCA did not make crypto safe. It made crypto predictable. For banks, that distinction matters more than any technological promise. The door is now open. And the institutions are walking through.